The Fed, Inflation, and Dollar Strength

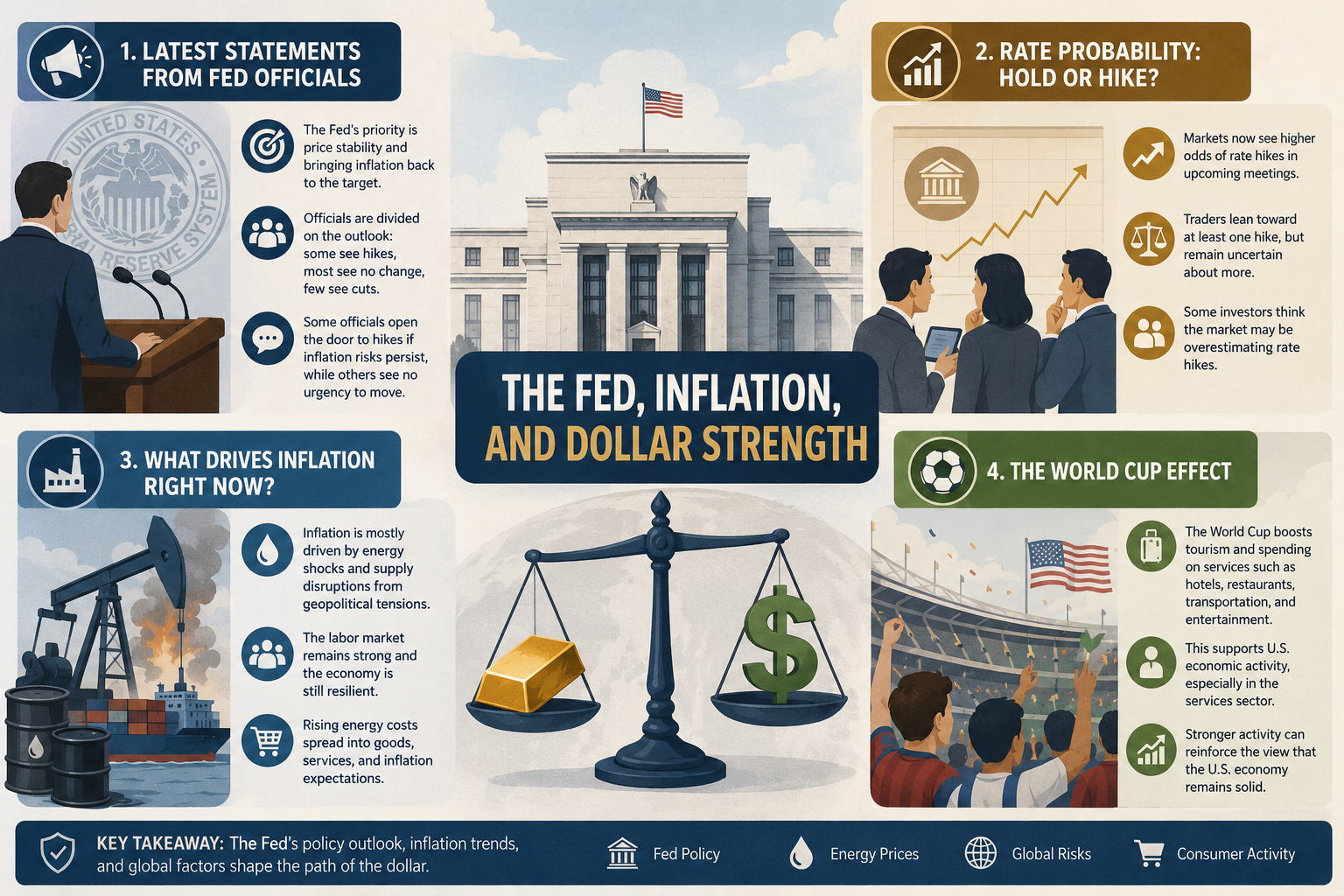

1. Latest Statements from Fed Officials

Federal Reserve Chair Kevin Warsh emphasized that the Fed’s main priority is to restore price stability and bring inflation back toward its 2% target. At his first meeting, the Fed kept interest rates unchanged in the 3.50%–3.75% range, but the latest projections suggested that rates could still move slightly higher before the end of 2026. Reuters also noted that Warsh has shifted the Fed’s communication style to be shorter and less dependent on forward guidance, leaving markets more reliant on incoming economic data.

According to the latest dot plot, 9 Fed officials expect an interest rate hike this year, 8 officials expect rates to remain unchanged, and only 1 official sees room for a rate cut. This marks a significant shift, as markets had previously been more focused on the possibility of rate cuts.

Several Fed officials have also opened the door to higher rates if inflation caused by the Iran war and rising energy prices becomes more persistent. Michelle Bowman said an energy shock could change her view on the rate outlook if its impact lasts into the second half of the year. Neel Kashkari also said that an immediate rate hike may not be necessary, but he is paying closer attention to rising inflation risks and the possibility that inflation expectations could become unanchored.

However, not all Fed officials are in a rush to raise interest rates. Mary Daly said there is no urgency to adjust policy rates and that the current policy stance remains in a good place. This means the Fed is not fully united on the need for a quick rate hike. Policymakers are still waiting to see whether inflation will remain persistent or begin to ease after the decline in oil prices.

2. Rate Probability: Hold or Hike?

According to CME FedWatch data cited by Reuters, the probability of a 25-basis-point rate hike at the July meeting rose to 36.3%, up from just 8.5% a week earlier. For the September meeting, the probability of a rate hike climbed to 69.1%, compared with 29.1% in the previous week. This shows how quickly market expectations have shifted after the Fed adopted a more hawkish tone.

Reuters also reported on June 25 that traders now see one rate hike potentially happening as early as October, with roughly a 50:50 chance of a second hike before the end of the year. In simple terms, the market is currently leaning toward at least one rate hike this year, but it is still not fully convinced that the Fed will deliver two hikes.

Still, there are different views among bond investors. Reuters noted that some asset managers believe the market may be too aggressive in pricing in rate hikes. Their argument is that inflation pressure could ease if oil prices continue to fall, energy supply normalizes, wage growth slows, and the housing sector remains stagnant. Citi even expects the Fed’s next move could be a 25-basis-point rate cut as early as October, while BofA forecasts three 25-basis-point rate hikes this year.

3. Is Current Inflation Caused by a Weak Economy or Energy Prices?

In my view, the current inflation pressure is driven more by energy shocks and supply disruptions caused by the war, rather than by a weak U.S. economy. The Fed still sees the labor market as relatively strong, with the year-end unemployment rate projected at 4.3%, lower than the March projection of 4.4%. GDP growth is projected to soften slightly from 2.4% to 2.2%, but that does not yet indicate a damaged economy or a recession.

Inflation pressure has risen sharply because of the war and higher energy prices. The Fed’s PCE inflation projection for the end of 2026 increased to 3.6%, from its March projection of 2.7%. Core PCE also rose to 3.3%, from the previous estimate of 2.7%. This suggests that the Fed is not only concerned about the direct impact of crude oil prices, but also about potential second-round effects on goods, services, and price expectations.

The conclusion is that today’s inflation is not mainly caused by a weak economy. Instead, it is being driven by energy and supply shocks that are occurring while the U.S. economy remains relatively strong. When an economy is weak, demand usually slows and inflation tends to ease. What is happening now is different: the economy remains resilient, energy prices surged, supply chains were disrupted, and the Fed is worried that these pressures could spread into core inflation.

4. The World Cup Effect

The World Cup currently taking place in the United States could also provide some support for the U.S. dollar, but only as an additional factor rather than the main driver. The biggest drivers of the dollar remain expectations of Fed rate hikes, safe-haven demand caused by the technology stock selloff, and weakness in other major currencies.

However, the World Cup may still offer a small boost through tourism, services spending, hotels, restaurants, transportation, and domestic consumption. S&P Global also noted that U.S. services activity in June improved partly due to the World Cup effect, while Oxford Economics estimated that additional hotel revenue in the U.S. market could approach US$900 million during the tournament.

In other words, the World Cup can indirectly support the dollar by strengthening short-term activity in the U.S. services sector. If services activity remains solid, the market may see the U.S. economy as still resilient, which could reinforce the view that the Fed has room to keep rates high or even raise them further.

Still, the World Cup is not the main reason behind the dollar’s strength. The dominant factors remain the Fed’s hawkish stance, inflation concerns, safe-haven demand, and pressure on other major currencies. The World Cup is only an additional supporting factor that strengthens the broader narrative of a resilient U.S. economy.

Source: Newsmaker.id