Hormuz Locked, Inflation Risks Regain Dominance

The harsh tone of Washington and Tehran on the 13th day of the war made one thing clear: the energy market is not seeing a "solution" anytime soon. US President Donald Trump's statements placing the Iranian nuclear issue above oil costs, along with Iran's new supreme leader, Mojtaba Khamenei, who wants the Strait of Hormuz to remain effectively closed, have led market participants to shift their baseline scenario from a temporary disruption to a more persistent risk.

At this point, the oil risk premium is determined more by physical transport capacity than by sentiment. The Hormuz closure disrupted millions of barrels per day, and the International Energy Agency called it the biggest hit to global production ever recorded. With the disruption at a logistical hub, the price response tends to be "jumpy" as the market reassesses effective supply availability, not just nominal production figures.

Oil surged more than 9% on Thursday, with Brent closing above US$100 for the first time since August 2022 and WTI hitting its highest closing level in more than three years, suggesting that administrative policy efforts have not broken the trend. Plans to grant temporary waivers to US domestic maritime rules and a second authorization for buyers to take Russian oil cargoes already at sea signal the administration's focus on the short-term supply side, but their impact is limited by the policy's "narrow" design and the fact that the primary bottleneck remains the security of shipping lanes.

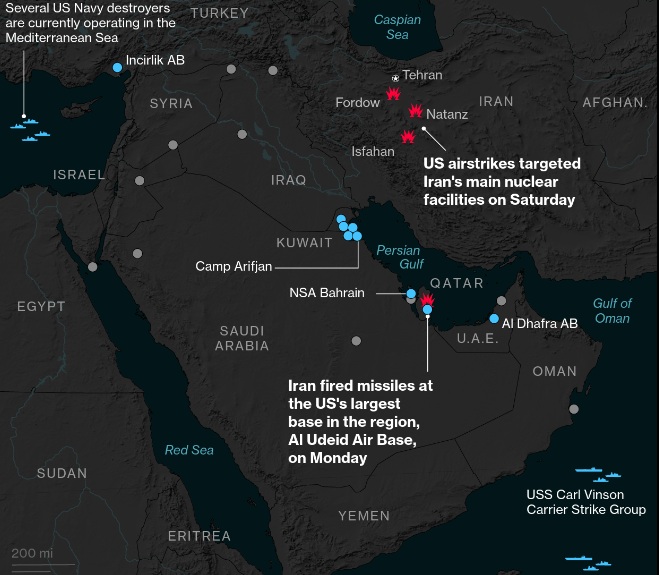

On the geopolitical front, the narrative of "measured escalation" has shifted to the risk of expanding fronts. Khamenei has raised the possibility of opening another front if US and Israeli attacks continue, while Israel continues its wave of large-scale attacks and Iran escalates attacks on Dubai and shipping assets. Attacks on three commercial vessels in the Arabian Gulf in the past 24 hours (according to UK Maritime Trade Operations) underscore the risk of disruption no longer being concentrated in Hormuz but potentially extending to other maritime routes and assets.

Cost and duration are now driving volatility. US officials have provided a detailed assessment that the first six days of the war cost more than US$11.3 billion, amid reports that some 6,000 targets have been struck since the operation began. These figures heighten uncertainty about operational stamina, the scope for political compromise, and how quickly the parties can de-escalate without losing their bargaining power, making it difficult for the market to place a final price tag on the conflict.

Additional risks arise from the maritime security dimension, which could shift logistical calculations from prohibitive to unfeasible. British Defense Secretary John Healey said Iran may begin laying mines in Hormuz, although Iran's Deputy Foreign Minister denied this. If the market becomes increasingly convinced that the mine threat is real, insurance costs, rerouting, and shipping delays could act as transmission channels that lock in high energy prices even before there is any physical damage to production facilities.

The market implications across assets are relatively clear: oil is likely to remain supported by a supply risk premium as long as Hormuz remains effectively closed and maritime disruptions persist, while gold could face a push-pull between two forces: geopolitical hedging demand, but expensive energy, raising inflation concerns and potentially curbing interest rate easing, which typically limits gold's upside. The dollar often benefits from a search for liquidity and safety in such conditions, especially if volatility increases. Its ultimate direction depends largely on whether the market places greater emphasis on risk-off or the negative impact of energy on global growth. (asd)

Source: Newsmaker.id