Gold Rises, Oil Wavers, Here's the Future Prediction!

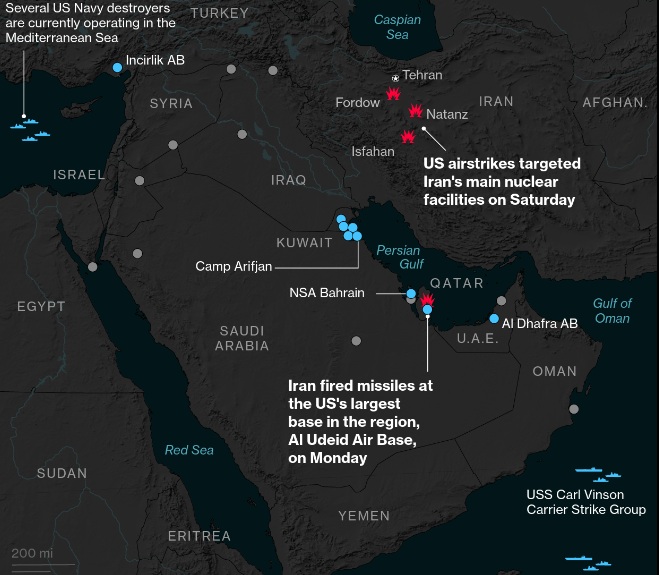

The conflict in the Middle East has once again become the focus of global market attention. The escalation of the war involving the United States, Israel, and Iran has market participants quickly seeking safe assets, while simultaneously reassessing the potential for disruption to global energy supplies. At the same time, the market is also beginning to weigh whether these tensions will persist or are beginning to de-escalate following the emergence of several conflicting political signals.

Amidst this situation, gold immediately received a strong boost as a safe haven asset. Gold prices briefly moved to around US$5,200 per ounce, indicating that investors still view the precious metal as a haven when geopolitical risks increase. This increase was driven not only by the war but also by concerns that protracted conflict could maintain high levels of global uncertainty for an extended period.

However, oil prices paint a more complex picture. After briefly surging to near US$120 per barrel due to supply concerns, Brent prices subsequently fell back to the US$87–88 per barrel area. This decline indicates that the market is beginning to ease its initial panic. This means the market is no longer solely focused on the threat of war, but is also beginning to consider the possibility of an emergency response from major energy-consuming countries to stabilize supply.

One factor pressuring oil is reports that the IEA is proposing the release of the largest strategic oil reserves in history. This discourse signals that if supply is disrupted further, member countries still have the tools to contain price spikes. Therefore, oil is no longer rising steadily even though the conflict is not over. The market is shifting between two narratives: on the one hand, the threat of supply disruptions, while on the other, there is hope that policy intervention can cushion energy price shocks.

From a monetary policy perspective, this situation places the Federal Reserve in a difficult position. Surging energy prices risk pushing inflation back up, but at the same time, previous employment data has shown signs of economic weakness. Reuters reports that the Fed is widely expected to remain on hold at its March 17-18, 2026, meeting, as it must balance the risks of inflation with slowing growth.

In this context, market attention is now focused on the February 2026 Consumer Price Index (CPI) data, scheduled for release on Wednesday, March 11, 2026, at 8:30 AM ET (approximately 7:30 PM WIB). This data is crucial because it will provide an indication of whether inflationary pressures are easing or intensifying. If inflation is higher than expected, the market could become more confident that interest rate cuts will be delayed. Conversely, if inflation is softer, expectations of interest rate cuts could strengthen again, giving gold room to remain strong.

Given all these developments, the market is currently in a highly sensitive phase. The short-term forecast is that gold has the potential to remain strong as long as the Middle East conflict persists and if the CPI does not escalate too much, while oil will remain volatile due to the tension between supply risks and the discourse on releasing strategic reserves. As a result, global markets could continue to fluctuate: the dollar has the potential to strengthen if inflation is high, gold remains sought after if geopolitical uncertainty persists, and riskier assets such as stocks are likely to move more cautiously until the direction of the conflict and inflation becomes clearer. (asd)

Source: Newsmaker.id