Hot Geopolitics That Are Shaking the Market

1) Saudi-UAE Tensions in Yemen. Latest update (December 30, 2025): The UAE declared the end of its remaining troop mission in Yemen after a Saudi-led synchronized attack on the port of Mukalla, which was linked to weapons shipments to the southern separatist group (STC), close to the UAE. The Saudi attack triggered a crisis within the anti-Houthi camp itself—the pro-Saudi Yemeni side even declared a state of emergency and demanded the UAE's immediate withdrawal, while the UAE denied the weapons shipment allegations.

2) Russia–Ukraine: The peace process is getting tougher. On December 30, 2025, the Kremlin (via Dmitry Peskov) said Russia would "tighten/toughen" its negotiating position after accusing Ukraine of sending dozens of long-range drones to a presidential residence in the Novgorod region (Russia said 91 drones). Ukraine denied the accusations, calling the accusations "fabricated" to justify escalation. The bottom line: this moment comes at a time when peace talks are in full swing, so tensions are rising again. 3) US–Venezuela: Pressure levels rise (blockade + attacks). In recent weeks, Washington has been increasing pressure on Nicolás Maduro's regime: Trump ordered a "blockade" of oil tankers entering/leaving Venezuela (specifically those on the sanctions list), and a series of ship interceptions/seizures disrupted Venezuelan exports. Then, the latest update at the end of December: Trump confirmed an attack on a docking facility allegedly linked to drug trafficking; media reports said the operation involved US intelligence elements. This chronology makes Venezuela's supply situation even more "vulnerable to surprises."

4) China–Taiwan: Largest exercise yet, clear signal. Update December 30, 2025: China held its most extensive military exercise around Taiwan, titled "Justice Mission 2025," including hours of live-fire and simulated blockades and air-sea operations. Beijing called this a response to US arms sales to Taiwan; Taiwan condemned it, and external parties (including Europe) contributed to destabilizing the region. Chronologically, tensions in the Taiwan Strait are always sensitive—once there's a trigger (weapons, visits, or statements), large-scale exercises are usually used as a "warning."

5) Mexico raises tariffs—China is the hardest hit. Starting Thursday, January 1, 2026, Mexico imposed significant tariff increases (mostly up to 35%) on imports from countries with which Mexico does not have FTAs, including China, India, South Korea, Thailand, and Indonesia. Thousands of products were affected (automotives, textiles, plastics, steel, etc.). President Claudia Sheinbaum stated the goal was to protect domestic industry and jobs and increase government revenue; but many analysts believe this move was also an attempt to "level ranks" with the US ahead of the USMCA review.

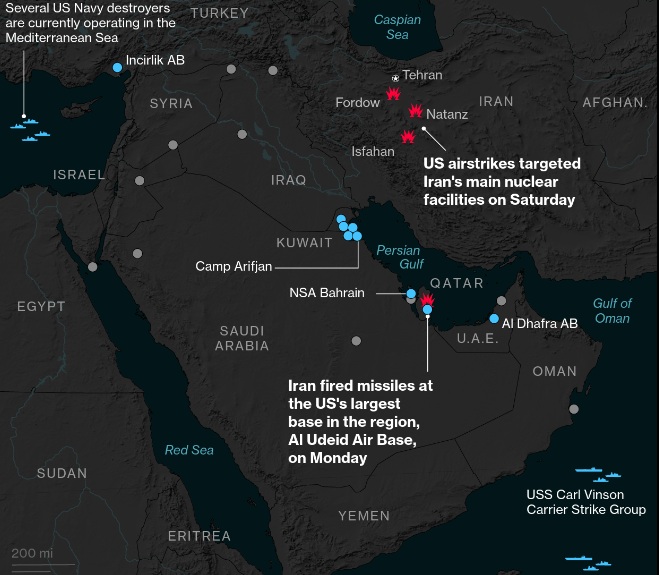

6) Iran: Economic protests + threat of external escalation. Update December 30, 2025: The Iranian government offered dialogue after widespread protests caused the rial to plummet to a record low and the cost of living to plummet. President Masoud Pezeshkian asked the authorities to accommodate demands deemed "legitimate." At the same time, external tensions are rising as Trump reiterates a warning about the possibility of a strike if Iran is perceived to be reactivating its nuclear capabilities—Pezeshkian responds by stating that Iran's response will be "harsh." The combination of domestic crises and external threats has revived the Middle East risk premium.

7) Red Sea: Trade routes are beginning to "test," but not yet normal. Update December 19, 2025: Maersk reports that one of its vessels successfully navigated the Red Sea/Bab el-Mandeb for the first time in nearly two years—a test run after many companies avoided this route since Houthi attacks (starting in late 2023) forced ships to detour via the Cape of Good Hope. But operators remain cautious: one successful voyage does not guarantee a permanent safe route; insurance and security guarantees remain key before a "full return."

8) OPEC+ (January 4, 2026): The market is holding its breath on supply. The immediate focus for oil is the OPEC+ video conference meeting on January 4, 2026. Delegates' expectations: OPEC+ will likely maintain its planned pause in production increases in early 2026 due to concerns about a global surplus (oversupply) and slowing demand growth. Chronologically, OPEC+ had accelerated production recovery throughout 2025, but oversupply pressures led them to hold back the pace of increases for Q1 2026—and this decision became an "anchor" for oil sentiment at the start of the year.

Impact on gold, silver, and oil: A series of geopolitical risks (Yemen/Taiwan Strait/Iran/Russia-Ukraine/Venezuela + the Red Sea route issue) tends to make the market prone to risk-off mode, which typically supports gold as a hedge. Silver can also be boosted when safe-haven sentiment strengthens, but because silver is also an "industrial metal," it is more sensitive if the market begins to fear slowing global demand. While the price may be boosted by a risk premium (potential supply/transport disruptions), the increase is often "resisted" by the broader theme of surpluses and OPEC+ policies, which will be the dominant determinant of price action in early 2026. (asd)

Source: Newsmaker.id